The CDC Eviction Moratorium – What You NEED To Know

You may have seen recent headlines referring to an “eviction crisis”: The COVID-19 Eviction Crisis: an Estimated 30-40 Million People in America Are at Risk – The Aspen Institute Experts fear the end of eviction moratoriums could plunge thousands of people into homelessness – CNBC President Trump signed an eviction moratorium order that effectively bans […]

Sept 2020 Monthly Market Update – Podcast

0:00 landlords will still be permitted to evict tenants in certain cases such as instances which the tenant has destroyed property or poses a threat to health or safety of neighbors. This is a story about a dude named Lane moved to the mainland em, but one place to stay. And then one day […]

Get first access to deals with PreREO w/ AHP CEO Jorge Newbery

0:01 This is a story about a dude named Lane he moved to the mainland and bought one place to stay. And then one day he went try to rent them out. And then he became one real investor make 0:15 a simple passive cash flow listeners today we have George Newberry, owner and […]

How to Decide to quit your high paid W2 day job w/ Kyle Jones

See our quitting guide here – Simplepassivecashflow.com/quit 0:00 Matt no amount of motivation is going to change the way you feel. But if you can commit to yourself and honor your commitments and doing whatever you need to do to make sure that you reach your goals financially, then you have to reverse engineer how to […]

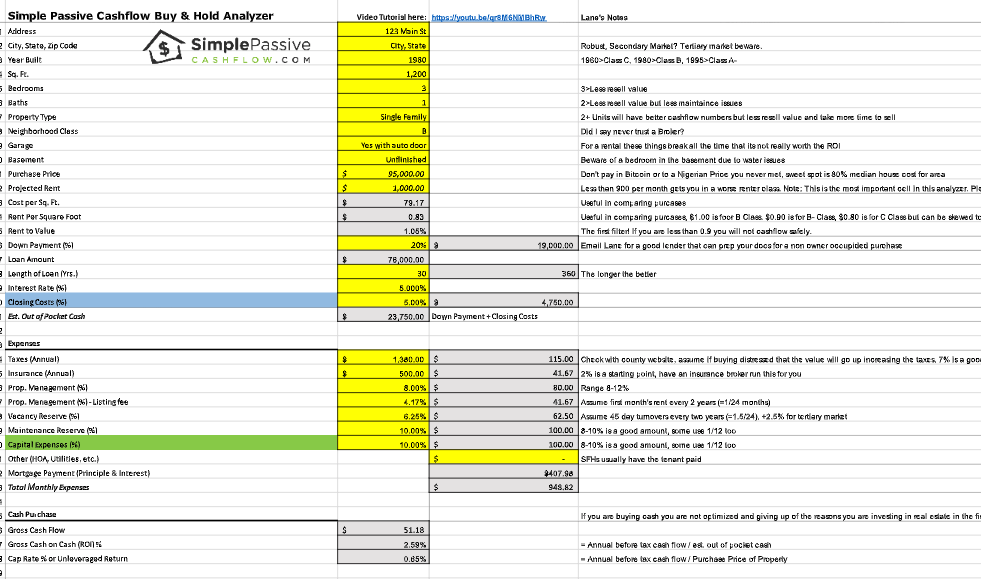

Single Family Home Rentals: Do you self-manage or use property management?

single family home rentals question here, these self manage them, or do you outsource some? I mean, a lot of people, at least in this tribe or passive investors, your highest and best use is likely at your day job or doing something else. Or if you have enough money, go and enjoy life. The […]

Section 280A – The Augusta Rule

Section 280A: TAX CODE (a) General rule: Except as otherwise provided in this section, in the case of a taxpayer who is an individual or an S corporation, no deduction otherwise allowable under this chapter shall be allowed with respect to the use of a dwelling unit which is used by the taxpay- er during […]

How the US Economy & Inflation Works w/ Russell Grey

You print too many dollars and people lose faith in the dollar. The only reason we’re able to pull this off is because we issue the world’s reserve currency and the whole world has to suck up all these dollars. The problem is if someone were to come along like a china and say, hey, […]

Repo Market Using COVID as a Cover-up? w/ Russell Grey (Part 1 of 2)

0:00 Introducing the new remote investor, incubator and ecourse we had the mastermind and we are going to break off from that being mostly an accredited investor group. And I wanted to create something that was helping out the little guy get started guys getting their first properties. And we’re calling this the incubator […]

How can I use part of my Roth IRA to buy passive income property?

How can I use part of my Roth IRA to buy passive income property, what you’re going to need to do to investor author is you’re going to need to probably move over to a IRA custodian that allows you to self direct. Now, a lot of these guys like Vanguard or fidelity was […]

Sheltering Capital Gains Without Painful 1031 Exchanges

So I’m cashing out some of my real estate that was inherited because the net income is very low given the asset value considering cashing out on a property that I bought 30 years ago in Arizona even though the rent ratio is amazing the income to asset ratio is low thought is to hold […]