YouTube Link: https://youtu.be/AT6x3ViRPos

Article Link: Text “simple” to 314-665-1767 to download the Hui Google Drive files and the 2018 Rental Property Analyzer

For a free electronic version of my bestselling book in 12+ categories text the word “ebook” to 587-317-6099.

Please help the show by leaving a review: http://getpodcast.reviews/id/1118795347

Join the Hui Deal Pipeline Club! SimplePassiveCashflow.com/club

Pardon the grammar – I’m an Engeneer, Enginere, Engenere… I’m good with math!

________Here are the Show Notes________

Graham Parham: New Awards:

- #1 in units at Highlands Residential Mortgage for 2017

- #11 in state of Texas and 92nd in the US according to The Scottsman Guide and

- Mortgage Executive Magazine – 1% top originators in the US

- Top Ranked – Ask A Lender

Discussion today is 1-4 unit income properties, not owner-occupied.

- 20% down on first ten financed properties? 25% for 2-4 units?

- DTI considerations when using HELOC from primary residence to invest?

- Credit scores down to 620. Max. credit score that helps?

- Reserves?

New Fannie Mae Reserve Requirements for Investors with Multiple Properties Owned

The Old requirements were six months Principle, Interest, Taxes, and Insurance (PITI) on the subject property and two on all other properties up to 4 leveraged 1 – 4 family properties excluding the primary residence. Properties 5 – 10 would require six month PITI on all properties.

The New requirements are based on a percentage of the unpaid principal balance on each loan excluding the primary residence.

- If a borrower has 2-4 financed properties, the reserves of 2% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

- If a borrower has 5 – 6 financed properties, 4% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

- If a borrower has 7 to 10 financed properties, 6% of the unpaid principal mortgage balances are required, excluding the principal residence and the subject property.

The aggregate UPB calculation does not include the mortgages and HELOCs that are on

- the subject property,

- the borrower’s principal residence,

- properties that are sold or pending sale, and

- accounts that will be paid by closing.

The subject property will still have monthly reserve requirements based on the total mortgage payment (PITI). Reserves are funds that you have access to liquid or non-liquid. Reserves are funds you need to have after the closing your transaction. Funds for reserves cannot be your funds for down payment or closing cost.

Fannie Mae now will allow for 100% of the Non-Liquid funds, not 60%

Non-Liquid funds can be used for reserve requirements.”

- IRA’s

- 401K’s

- SEP Funds

Gifts are NOT allowed on an investment property.

- Investor interest rates how much higher than owner-occupied?

- Mortgage sequencing. Example: if buyer wants to buy in Memphis today, Jacksonville next month, how should they plan?

- Overall, lending climate more lose or tighter than 1 year ago? 5 years ago?

- What should a prospective borrower do before contacting you?

- 1031 exchanges Cost and funding

- What cost are covered in the exchange

What is UP with interest rates?

4 Factors that determine your mortgage interest rate:

- Credit Score

Credit Scores Adjustments

- 740 +

- 740 – 720

- 720 – 700

- 700 – 680

- 680 – 640

- 640 – 620

- % of down payment 20% or 25%

- Loan Amount Adjustments

- Property Type

What about the 15 Year fixed?

Does it make since to pay points?

What is the difference between Mortgage Brokers and Mortgage Bankers?

What are overlays?

Does Fannie Mae have a black list?

Are Appraisals regulated and by who?

Is there an appraisal black list?

What happens if the appraisal does not come in a contract price?

Closing cost differences between lenders

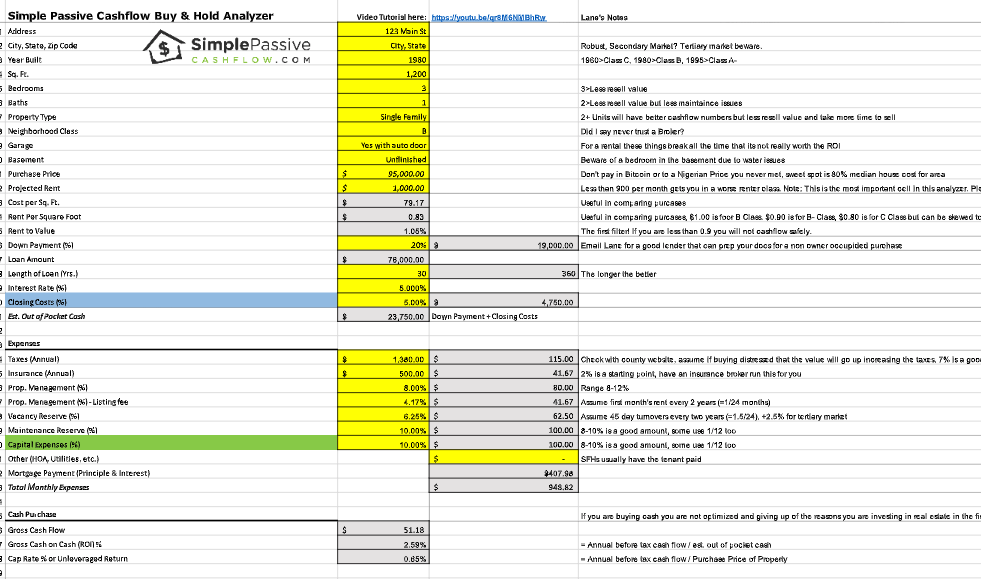

Should I pay cash for my investment properties or use leverage?

The next example will show the benefits of using 20% down leveraging for properties versus buying one property and paying CASH.

If you pay $150,000 in cash for one property, your net cash flow is $1245.00. By putting 20% down with an 80% loan to value and a 5% interest rate, your net cash flow is reduced to $600.81. Let’s not stop there. Keep in mind that 20% down payment on a $150,000 home is only $30,000. If you bought FIVE $150,000 homes and put 20% down on each with the same loan terms and monthly rents, you could increase your return on investment by $1759.05 a month to $3004.05. Invest your money wisely.

The net cash flows do not take into account the annual city, county and state property taxes and the annual hazard insurance. The numbers may vary considerately by the taxing authorities. You will have to include that information in your bottom line.

Graham W. Parham has been a Mortgage Loan Officer for over 18 years with 25 years

in sales and marketing. He is a leader of financial expertise in the North Texas

residential real estate market, developing a significant following among homebuyers

and investors. Known and respected industry-wide, Graham’s production consistently

ranks him as a top producer in this market place. According to Scottsman Guide

Graham ranked 92 nd in the US loan originators.

Graham offers invaluable insight into a purchaser’s likely requirements, providing an

exceptional business ethic of customer service and respect, catering to their needs from

pre-qualification to closing. He is a truly dedicated person, who strives to ensure that

each transaction is handled in a timely and stress free manner. By employing these

standards, Graham has established a solid reputation for going the extra mile to put

together the absolute best financing available for his clients. Graham prides himself on

staying ahead of the curve, keeping up to date with the latest products and industry

trends.

As an active investor himself, Graham has a strong insight on what his investment

buyers are looking for to accomplish their short and long term goals. Knowing that

investment loans strongly scrutinized, it is up Graham his team of underwriters who

understands rental property loans versus that of an owner occupied residence. His

general knowledge of REO properties and Turnkey providers coupled with a strong

operational staff allow his loan closings to be seamless and “On Time Every Time”

Highlands Residential Mortgage, LTD. is completely submerged in the real estate

investing industry and has access to many lenders nationally. Our clients benefit from

up to date guidance on all conventional investor loan programs, and less known

creative financing strategies. Knowing that an investment loan will be far more

scrutinized, it is Graham Parham and his team of underwriters who understand a loan

processed for a rental property versus that of an owner occupied residence.

Just as you would not seek legal counsel from someone who does not have a law

degree, nor should you trust a loan originator for your investment property loan from

someone that is not an investor themselves. Highlands Residential Mortgage, LTD. is

an unparalleled mortgage lender whose delivery sets us apart!

Graham Parham’s team mission is to consult every investor based on those

individualized situations and goals. Whether you are buying your first home or

investment property, we carefully look at your options that will give you the best

opportunity for success. Because we know how important your investment financing

strategy is, our extensive research and knowledge of those programs will be brought

forward in educating you as an investor, throughout the lending process.

“My goal is to continue assisting my clients for life and help them meet the ever-

changing needs life throws our way!”

To get access to the lending guide please sign up below:

is