Dumping your 401k, Helocs, 529s, IBC, Spouse Help Accredited Investor Coaching Call

Hey, simple passive cashflow listeners. Today, we are going to be doing a coaching call where the topics are going to be withdrawing money from your 401k. Should you do a 5 29 plan for college savings? If not, what should you do? And a little bit review on infinite banking. I know a lot […]

Travel Hacking with Geobreeze Travel

Aloha everybody! Those of you guys who’ve been following me for quite a while, it’s been a journey from 2016, doing this podcast. I have always been interested in the financial blogs sphere, podcast space. It was early when I started to read all these financial blogs. Back then it was silly things like which […]

Creating Community With ApartmentLife.ORG

Hey, simple passive cashflow listeners. Today, we are going to be talking about something we’re doing on a lot of our properties and some tips for you landlords out there to increase the community at your properties. Ultimately, it’s going to lead to higher rents and better revenues for you guys. If you guys haven’t […]

Scarcity to Abundance with “Money Honey” Rachel Richards

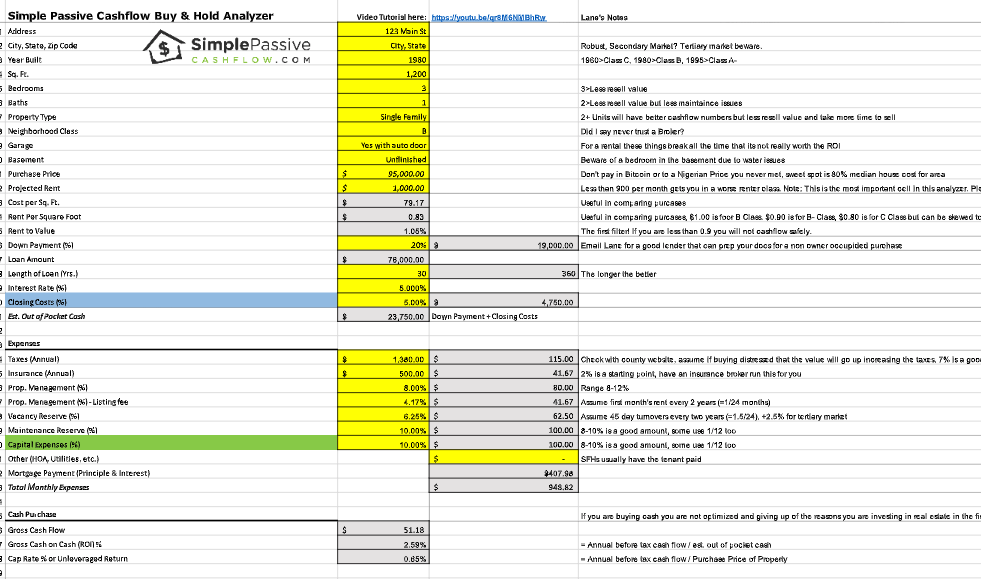

Coaching Call with a Million Dollar Investor (Chris)

On today’s podcast we’re going to be doing a coaching call but a little bit of announcements. We’re going to be unveiling the new Infinite Banking e-course. I put this together to get all our questions on infinite banking. I think a lot of you guys listen to this stuff on a podcast and you […]

The Practice of Groundedness with Brad Stulberg

hey, simple passive cashflow listeners. Today, we are going to be talking with Brad Solberg, who is dropping his book It’s releasing this week, the practice of groundedness. We’d like to take a break from the real estate investing tax legal. Infinite banking, which by the way, we’re also dropping the infinite banking e-course this […]

September 2021 Monthly Market Update

Welcome everybody. This is the monthly market update for September, 2021. If you guys want to check out past episodes, you can go to simple passive cashflow.com/investor letter, and we are going to be going over some teaching points and some articles that I’ve stumbled across over the past. Some freebies for you guys, if […]

Fun Story – Operating/Investing ATM Machines

hey, Simple Passive Cashflow listeners. Today, we have a simple passive cashflow who we deal pipeline club member. Who’s invested in some deals and has an absolutely crazy story to share with you guys. Now, the people that sign up for our group and especially come out to our events are definitely not average. I […]

Quick Announcements + Special Events + Intro to Infinite Banking

This is a special announcement. We are doing a special webinar on September 4th we’ll try and get it done in a couple of hours in a cram school type of format, where we go over the infinite banking policy. A lot of you guys had a lot of questions and we’re going to be […]

Near Death Experiences with Kathy McDaniel

Hey, simple passive cashflow listeners. Today, we have Mary McDonald here who is an author of a great book that you could find on Amazon called misfit and hell to heaven. Ex-pat so the reason why we are bringing. Mary onstage is because we like to do one of these touchy feely podcasts, know, maybe […]