I am sure someone somewhere is trying to invest in something similar and fooling themselves that they are making money on the project. But you are smart and you subscribe via RSS feed to this blog and podcast

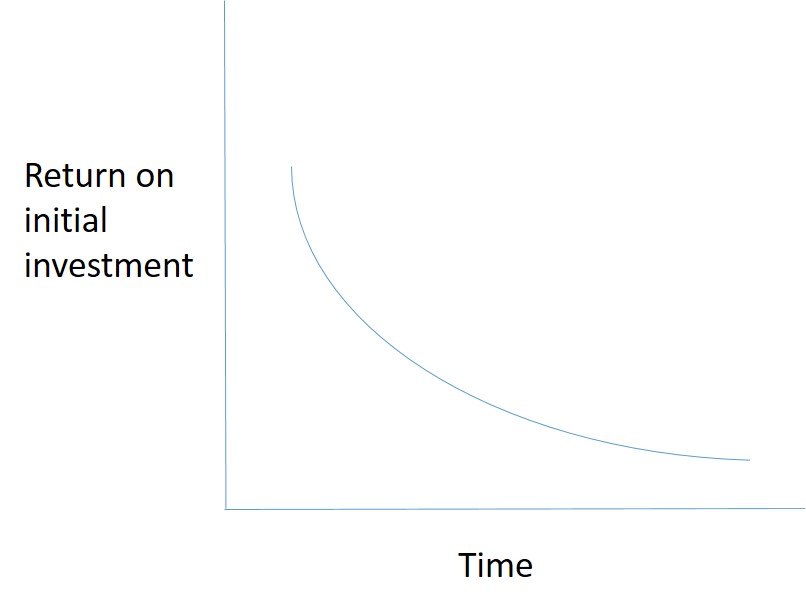

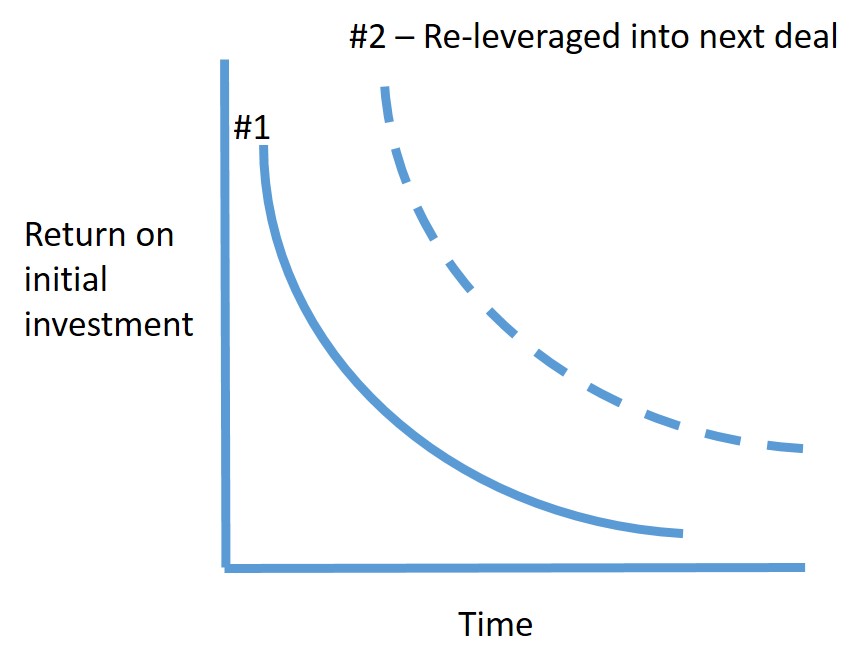

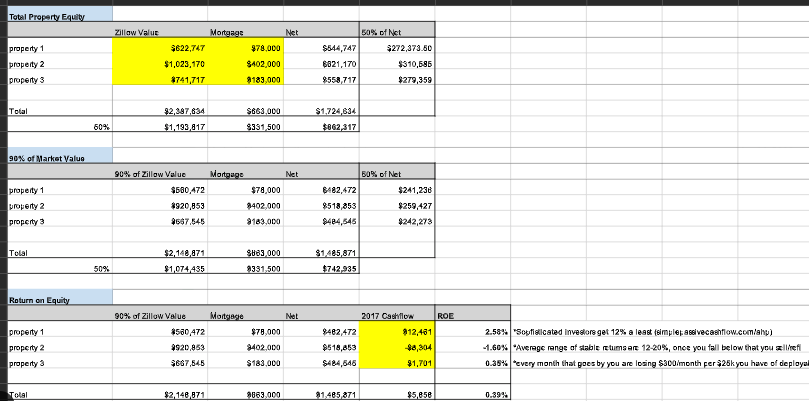

Long story short, I decided to sell these rentals to unleash this “lazy money” and get it working again with prudent leverage. This is what separates sophisticated investors who look at the numbers and your mom & pop investors who go by warm & fuzzy feelings of “hey I’m making cashflow, life is good”. Yes, Mom you are cash flowing but that is because you are halfway to 100% cash in the deal and you are taking on all that hassle and risk for a microscopic return.