Looking for a good CPA?

If you would like a referral to the team that we use please click this button, complete the form, and we will be in contact with in 2-3 business days.

If you would like a referral to the team that we use please click this button, complete the form, and we will be in contact with in 2-3 business days.

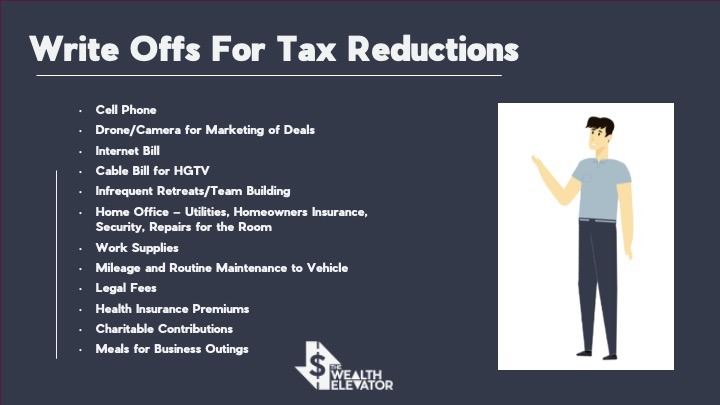

In the world of real estate investing, understanding the nuances of taxes is crucial for optimizing returns. One key aspect that demands attention is depreciation recapture. In this article, we’ll delve into the basics and strategies around managing depreciation recapture, with insights from both an experienced investor and a CPA.

Ordinary vs. Passive Income:

The journey starts with distinguishing between ordinary and passive income. While ordinary income is subject to various taxes, the goal for investors is to transition to passive income, generated without active involvement and benefiting from different tax treatments. This transition is often facilitated through leveraging depreciation and passive activity losses (PALS) in real estate.

Depreciation Basics:

Depreciation involves deducting the cost of property improvements over time. The red portion of a property, representing improvements, is depreciable, while the green portion (land) is not. Single-family homes allow for depreciation over 27 years, but larger deals benefit from cost segregation studies, accelerating depreciation for components with shorter lifespans.

Cost Segregation Studies:

Cost segregation studies break down property components for faster depreciation. While larger deals justify the cost of these studies, caution is advised against cheaper, potentially unreliable alternatives. A good study allows for front-loading depreciation, offering immediate tax advantages.

Understanding Passive Activity Losses

PALS are derived from the improvement portion of real estate and play a pivotal role in offsetting passive income. Investors can strategically utilize PALS to minimize tax liability and enhance overall returns.

Real-Life Examples:

Real-life examples illustrate how depreciation and PALS impact investors. A case study involving a Texas property showcases the significance of accelerated depreciation. While depreciation recapture becomes inevitable upon selling, the benefits of taking depreciation upfront can outweigh the future tax implications.

Tax Implications at Exit:

Upon selling a property, investors face three tax considerations: long-term capital gains, recapture tax, and ordinary income tax. Long-term capital gains are taxed at 15%, recapture tax (25% max) applies to stored-up passive losses, and ordinary income tax accounts for the remainder. Bonus depreciation can lead to upfront tax savings, providing an edge even with future recapture.

Navigating depreciation recapture requires a strategic approach. Investors must weigh the benefits of immediate tax advantages against future recapture liabilities. Building a relationship with a knowledgeable CPA is crucial for making informed decisions and optimizing tax strategies throughout the investment journey.

Remember, the world of real estate taxation is nuanced, and individual circumstances vary. It’s advisable to seek personalized advice and stay informed about changes in tax laws that may impact your investment strategy.

***Remember, tax laws are complex and subject to change, so it’s crucial to seek advice from a qualified tax professional who can provide guidance tailored to your specific situation and the current tax laws in your jurisdiction.

In one of my former podcast episodes, I sat down with former IRS special agent Robert Norland shared valuable insights into the IRS’s criminal investigation division and shed light on crucial aspects of tax strategies and legal pitfalls to avoid.

The IRS’s Specialized Role:

Norland highlighted the unique position of the IRS in dealing with tax crimes, explaining that the agency’s criminal investigation division is solely responsible for investigating tax-related offenses. Unlike other law enforcement agencies such as the Secret Service, DEA, FBI, or Homeland Security, the IRS has exclusive jurisdiction in tax crimes. Out of the IRS’s vast workforce, approximately 2,000 individuals are designated as criminal investigators, operating at a level comparable to other specialized agents in law enforcement agencies.

Intersection of Law Enforcement and Accounting:

Drawing from his experience, Norland emphasized the marriage between law enforcement and accounting within the IRS’s criminal investigation division. Special agents utilize their accounting skills to track tax evaders and money launderers globally, making them the world’s financial investigators.

Tax Strategies and Audits:

The discussion touched upon common tax strategies, such as real estate professional status, where individuals may attempt to use passive losses to offset their adjusted gross income. Norland cautioned against common misconceptions, such as obtaining a real estate license as a means to claim real estate professional status. He explained that the IRS primarily functions as a collector and assessor of taxes, assessing situations and determining tax dues.

Civil vs. Criminal Investigations:

There is a critical difference between civil and criminal investigations. In civil cases, the burden of proof is on the taxpayer to demonstrate the legitimacy of deductions or losses. However, in criminal investigations, deductions are automatically assumed until the government proves willful intent beyond a reasonable doubt. Norland provided examples to illustrate that while discrepancies might be scrutinized in civil cases, criminal investigations typically focus on substantial tax losses and intentional evasion.

Thresholds for Criminal Sentences:

Addressing concerns about potential criminal charges, Norland explained that the sentencing guidelines for tax-related crimes do not specify a dollar limit. However, he emphasized that criminal investigations usually target cases with significant tax losses, ranging from $40,000 to $50,000 or more.

Distinguishing Tax Evasion and Tax Avoidance:

Norland clarified the distinction between tax evasion and tax avoidance. Tax evasion involves intentionally avoiding paying owed taxes, whereas tax avoidance is the legal practice of minimizing tax liability through legitimate means.

The crux of tax evasion versus tax avoidance often hinges on the element of willfulness. Tax evasion involves intentional wrongdoing, where individuals knowingly engage in fraudulent activities like falsifying documents, maintaining second sets of books, or providing misleading information to investigators. Willfulness is about knowingly doing the opposite of what is right. It extends beyond mere mistakes and requires an intentional deviation from tax regulations.

IRS audits aren’t triggered by innocent errors, such as a transposing mistake in a tax return. The focus is on matters of material importance, where intentional actions significantly deviate from tax norms. This might include adding zeros to deductions or engaging in deceptive practices, like maintaining a second set of books. The willful nature of such actions becomes a red flag for IRS scrutiny.

The likelihood of getting flagged or audited by the IRS is relatively low, often ranging from 1% to 2% based on income levels. Audits usually begin with a letter addressing a mismatch of information on a tax return. This might involve unreported transactions, such as a property sale absent from the tax return but documented in the IRS system via a 1099 form.

Most audits or IRS correspondence stem from a mismatch of information, signaling potential discrepancies in reported income or deductions. However, in some cases, a tax return might be pulled for audit based on various factors. Auditors are trained to identify “badges of fraud,” including suspicious documentation, false records, or consistently questionable financial activities. When such flags arise, the IRS may escalate the matter to a criminal investigation.

When faced with an IRS inquiry, individuals often contemplate seeking professional help. While smaller discrepancies may be addressed without professional assistance, the decision hinges on a cost-benefit analysis. For more substantial tax issues, involving a qualified tax professional becomes crucial, especially as audits progress from a simple mismatch letter to a comprehensive review of the entire tax return.

Recent headlines about the IRS hiring an “elite force” of armed agents caused considerable concern. However, the reality is more nuanced. The IRS, facing retirements and attrition, needs to replenish its workforce to maintain tax compliance. The alleged 87,000 armed IRS agents, as propagated in some reports, is a gross misrepresentation. In truth, there are only around 2,000 special agents with firearms, and their recruitment and training are meticulous processes.

While tax compliance is a necessary aspect of a functioning society, it’s essential to understand the intricacies of IRS investigations. From willfulness in intentional tax actions to audit triggers and the probability of getting flagged, navigating the IRS landscape requires a careful understanding of tax laws. Seeking professional guidance becomes paramount, especially when audits progress beyond initial correspondence. In essence, maintaining a balance between tax responsibility and informed decision-making is key to a hassle-free tax experience.

My name is Lane Kawaoka, and I hope my blog/podcast will help families realize the powerful wealth-building effects of real estate so they can spend their time on more important, instead of working long hours and worrying about their financial troubles. There are a lot of successful families with good jobs (teachers / engineers / programmers / finance) yet they struggle to make ends meet financially. It is their kiddos who ultimately get the short end of the stick. Being a Latch-Key Child growing up, both my parents had to work and I was left home alone after school to fiddle with my thumbs.

With Real Estate you are able to grow your wealth exponentially faster than the conventional 401K’s and stock investing, therefore you are able to escape the dogma of working 50+ hour weeks at a job that is unfulfilling. And if you are one of the lucky ones who happen to do what you enjoy… well good for you 😛

Money is not everything but it is important because it gives you the freedom to live life on your terms.

Annoyed by the bogus real estate education programs out there (that take money from people who don’t have it in the first place), I set out to make this free website to help other hard-working professionals, the shrinking middle-class. I hope to dispel the Wall-Street dogma of traditional wealth-building, and offer an alternative to “garbage” investments in the 401K/mutual funds that only make the insiders rich. We help the hard-working middle-class build real asset portfolios, by providing free investing education, podcasts, and networking, plus access to investment opportunities not offered to the general public.

“The true meaning of wealth is having the freedom to do what you want, when you want, and with whom you want.

Building cash flow via real estate is the simple part. The difficult part occurs after you are free financially to find your calling and fulfillment.

But that’s a great problem to have ;)”

excerpt from The One Thing That Changed Everything