CHEAPER Third Party Collateral Loans for Your Infinite Banking

What’s up investors now on today’s podcast. We’re going to be talking about a little bit of an advanced topic on infinite banking, a little trick that the folks in the HUI have found and have been utilizing to get a little bit better interest rates on the cash value portion of their life insurance. […]

Pruning your rentals + Outsouring debt with Enrich Author Todd Miller

Now on this podcast, you’re going to be hearing me interview an author that wrote about, enriched about building wealth over time. There were a few things in this interview that I clashed over. Here’s the thing, like a lot of these authors, it’s nothing to take much to write a book these days. I’ve […]

College Admissions Strategy: What Most Don’t Know About

Hey simple passive cashflow listeners. Now, today we are going to be listening to a podcast they recorded a while ago, as many of these podcasts are. So if anything happens to me and I die, they’ll probably be simple, passive cash flow podcasts going on for another year and a half. So just in […]

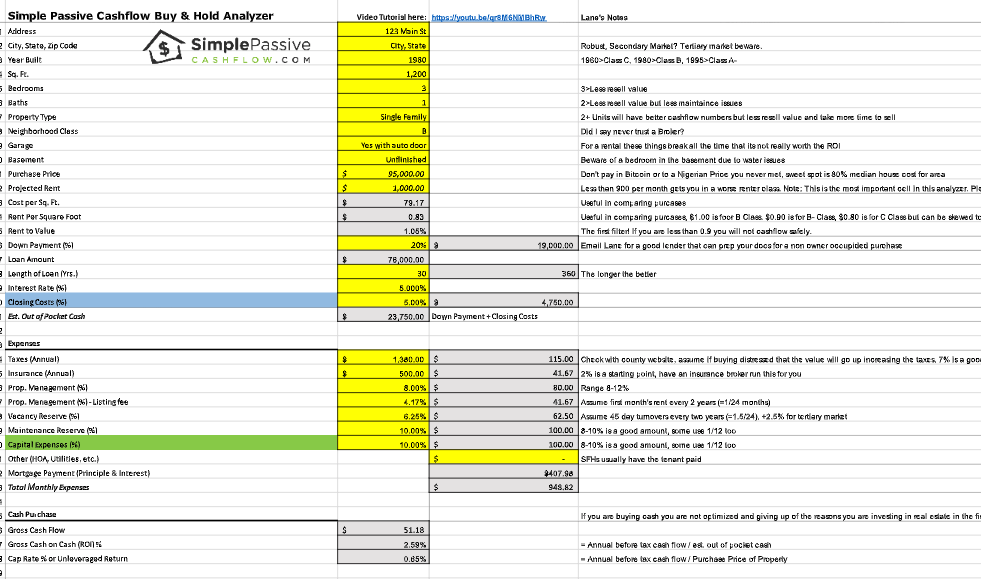

Coaching Call – 4M Engineer getting started

What’s up investors? We’ve got a really cool coaching call with a little bit higher net worth investor today, 4 million. And I think it’d be good that a lot of you guys who are on the road to financial independence check out all the coaching calls and what I would recommend. And we have […]

May 2022 Monthly Market Update

Hey folks. This is the monthly market update where we are going to be going through all of the important articles and packing investors these days. If you haven’t yet checked out my book, the journey to simple passive cashflow, I think it’s like less than a hundred pages. It should be a […]

How to Add “Play” in Your Life

Hey simple, passive cash flow listeners. We are taking a break from the regular hard investing tax, legal podcasts, topic matter and talking a little bit about something that enriches all your guys’ souls out there. Something that I’ve been attuned to since starting the podcast actually, and getting into a lot of personal development […]

What Success Means to Lane Kawaoka

Hey simple, passive cash flow listeners. Today, you’re going to be hearing a pretty good interview that somebody had done on me and just, something that’s been going on in my life is looking for purpose, financially free so early, like many of you, you start to ask the question. After when is enough […]

Raj Interviews Lane | Real Estate Investing for Working Professionals

What’s up simple passive cashflow listeners. Today you’re going to be hearing an interview that I actually thought was pretty good. I go on a lot of these interviews and there’s a lot of lame podcasts and a lot of, even lamer podcasts hosts that just don’t ask very good questions and put me to […]

April 2022 Monthly Market Update

What’s up everybody. This is April 2022 monthly market update where we go over some of the highlights that I saw from the news this week and a little bit of commentary, not too much politics. Cause I think that’s a little bit of a waste of time. But it’s sometimes fun to talk about, […]

Coaching Call – Remote Investor Incubator Student Round Up

What’s up everybody? This is episode 300. We’re going to be doing a little giveaway if you guys stay to the end of this, but where we’ve been in the past, what we started this podcast in 2016, and back then I was still buying little single family homes. Obviously, you know, I came in […]