Coaching Call: From 400K To $1.4M Net Worth in 2 YEARS + Ditching The Rentals!

What’s up simple passive cash flow? This week’s podcast, we are going to be talking to another coaching call. This guy’s got 1.4 million net worth and he is finally ditching the rentals. Now, I would say most of you guys who are investing with us these days, maybe not the vast majority, but. Little […]

Family Estate Planning Toolkit

https://youtu.be/hziEsxMVF6w Get FREE access to my Family Estate Planning Toolkit First Name* Email* Phone Please verify your request* Submit

Syndication Lite Ecourse

Get FREE access to my Syndication Lite eCourse here! First Name* Email* Phone Please verify your request* Submit

AMA

https://www.youtube.com/watch?v=J8Yl1qWg1c0 Tired of the steep tax you’re paying, as a professional, and you want more cashflow in which you can benefit from? Or you’re thinking of diversifying your investments and plan to try real estate investing? Come Ask Me Anything about how I got to over $1 Billion Current AUM and over 7500+ Doors. […]

Getting Your First Rental Property

Tired of the steep tax you’re paying, as a professional, and you want more cashflow in which you can benefit from? Or you’re thinking of diversifying your investments and plan to try real estate investing? Imagine if you can rapidly jump into being a passive investor. Focusing on what others failed to do that if […]

Why Investors Must Consider Real Estate in Huntsville Alabama

As of today, half of the year 2021 has passed. Though there is presence of COVID- 19 vaccine in the market, uncertainty in what things may come and in the real estate industry still never left. While we cannot eliminate the presence of uncertainty in our lives and what lies ahead, these two indicators drive […]

Why Invest in Houston Texas

Houston, Texas is one of the hottest real estate markets in the country right now, luring droves of newcomers from California, the northeast, and other pricier real estate markets. From 2017 to 2018, the Houston area saw an average of 250 people moving to the region every day, a trend that has stayed mostly on […]

Should You Use an LLC?

Everybody thinks that they’re super protected with an LLC, right? Why all being Abada tell us like the dark side of these LLCs, are they truly Bulletproof there’s there? There’s nothing. That’s truly Bulletproof, especially if it’s purely domestic, like whatever you create, eventually, if you get to a high net worth. So like you […]

How to Increase Tax Deductions on Single Family Homes

So DIY cost sag is a platform we developed after being in the industry since 2002 and doing well over 15,000 studies. And we saw a need in the market for smaller properties under a million dollars. And whether it’s a single family, residential, duplex, quad, or triplex. We cover those, or it might also […]

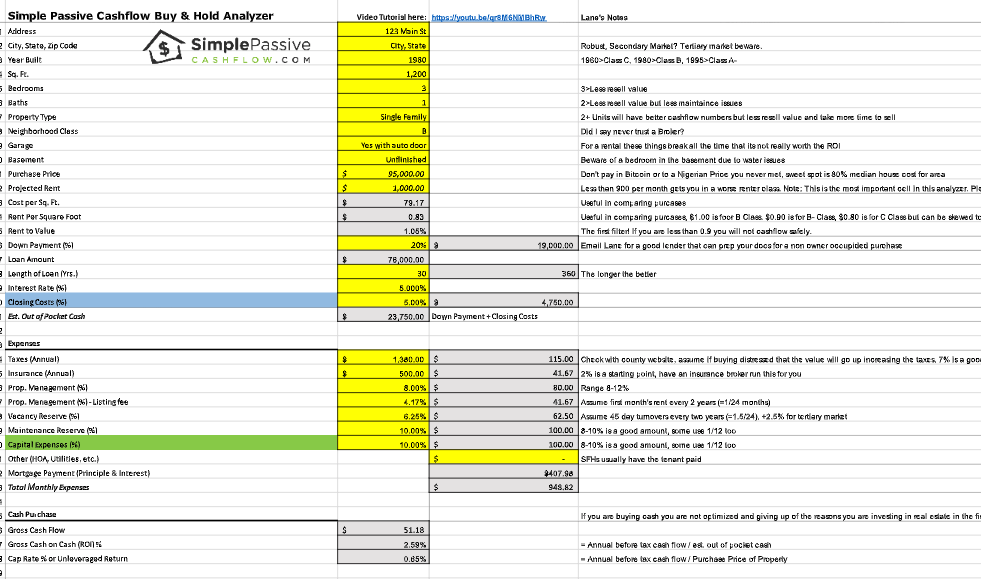

How Much Should My Rental Property Cash Flow?

What cash on cash return would you recommend for a single family home rental property where the goal is cashflow not appreciation? So normally, I think least 8% return is what you’re trying to shoot for. So if you’re using an analyzer, what I would put in there and make sure you’re also including all […]